Summary

Fuck the British tax system. And the student loan system too, whilst I’m at it.

Views my own. Discussion ≠ endorsement. Do try this at home.

Steal All My Bananas

Photo by the author

~3,900 words

Published:

Last modified:

Fuck the British tax system. And the student loan system too, whilst I’m at it.

In the previous UK financial year, I earnt the princely sum of £9,500 in UK-taxable income (due, in no small part, to moving abroad in the summer). This was to be all covered by my Personal Allowance of £12,500-ish per year, and so my total taxable amount should have been nil.

So why—the fuck—did I just have to lend the taxman seven thousand pounds?

The UK is a deeply silly country, in ways that I find increasingly aggravating the longer I live outside of it and realise just how optional it all is.

For example, to explain why our tax calendar runs from April 6 to April 5 would require a discussion on the vagaries of a calendar change 500 years ago—this is literally not a joke, but the insistence on continuing on in this manner can only be described as self-harm.1 The end result is that, having now moved to a far more sensible and thoroughly metric sort of country with a tax year aligned to the calendar year, I am left trying calculate my figures between three disjoint periods: the 2024–25 UK tax year; the 2024 French tax year; and the 2025 French tax year (which I don’t even have final figures for, and won’t do so until around August).

On top of that, I am having to learn an entirely new tax system (my third!) from scratch, in a language I can only somewhat read, in a very short one-month window. Because this is my first French return, and because I need to tell the UK authorities that I’m moving abroad, both returns need to be written out by hand and submitted by post.

Let me repeat that, as foreshadowing for the level of bullshit to come: HMRC require me to physically post them a letter to tell them that I’m no longer in the country.

Anyway, I cracked on, deciphering page after page of cryptic French tax guidance and learning about all manner of different forms (at least twice discovering a completely new and utterly crucial one when I thought I was done which changed everything and made me start again from scratch).2 The UK forms I was a little more familiar with, although only through the online tool prior to now, and I gradually pulled everything together. ‘SRT’, ‘DTAs’, ‘Schumacher non-residency’: just some of the new concepts I had to wrap my head around, for having had the temerity to live a slightly abnormal life.

I dotted all my ‘i’s, crossed all my ’t’s and sent off my French return in May, and then my UK return whilst visiting in June, along with requests to both countries’ tax authorities for proof of residency.

In the end, despite moving to France full-time in May and getting my titre de sejour in July, because of my frequent trips back to the UK (with 131 days to France’s 235, across 4 separate visits) I was ineligible for split-year treatment and instead had to dig down into the UK–France Dual Taxation Agreement (DTA), eventually deciding that because every prior test was inconclusive, I would just have to break the tie by nationality for this year and remain UK tax-resident (but still enjoy all of the French tax breaks—that’s that Schumacher residency magic, baby!).

As I made clear to HMRC, though, most of my figures would be provisional until later that year, and the final quarter will remain provisional until later this year; also, that my lingering UK tax residency in 2024–25 was a fluke and would not be the case in the following year.

At the start of October, I received my French tax statement for 2024: rien à payer (as expected, since all my pay had been taxed at source). Later in the month, I received my UK tax statement: £6,840.10 due by January 31st, with an additional £1,505.70 due by the end of the following July.

Welp.

Suffice it to say, this was rather steeper than the zero pounds I had been expecting, so I got back to work: checking my now-final French payslips; cross-referencing figures; converting between currencies; and re-reading all the guidance. I realised that I had overstated my taxable foreign income by about £7,000 (because I had just used the gross income figure), and I understated my foreign tax already paid by about £2,500 (because France has six different types of deduction that all count as income tax under the DTA).3

Not to worry: I had already told HMRC the figures were provisional, so presumably I’d be at the front of the queue for processing updates when I finally received my real numbers. I figured I’d just send in an amended return and that it’d all get sorted before the end of January, and so I posted the amended return (recorded delivery, of course) at the end of November, during another visit back, and didn’t think much more about it.

And for good measure, I included another reminder that in the 2025–26 tax year, I would be fully France-resident.

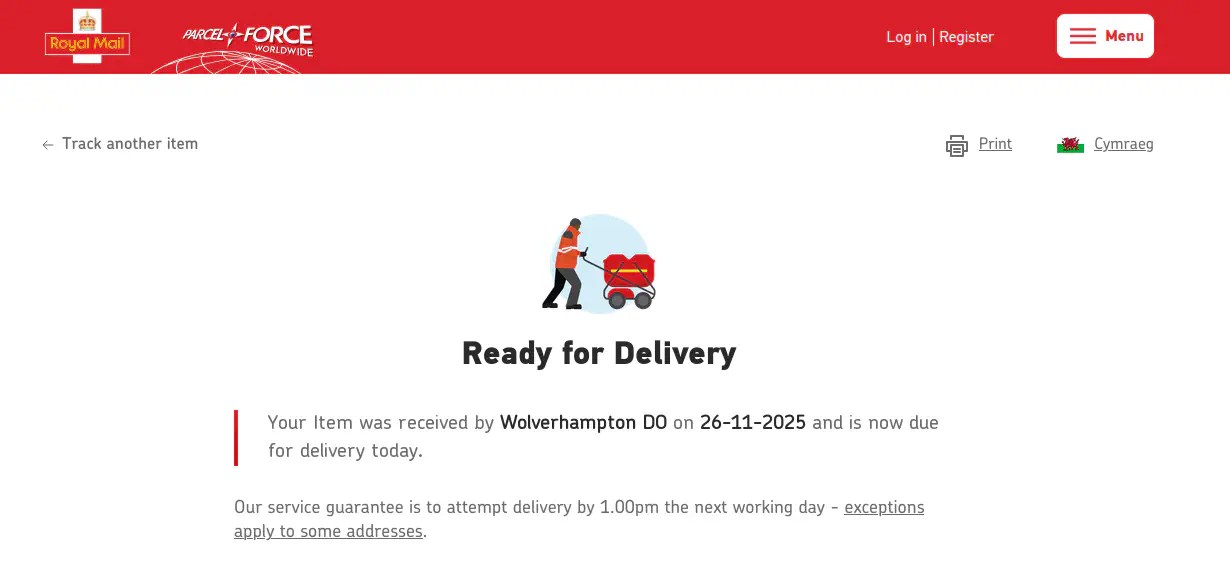

Time passed and, after recovering from my new year’s celebrations,4 I remembered about the looming end-of-January payment deadline and realised I hadn’t heard anything back from HMRC yet. I took a look at the HMRC online portal, and they were still asking for both the arm and the leg. Hmm…

I still had my postage receipt, so I plugged the reference number into the Royal Mail tracker, only to find that my amended return had been seemingly abandoned in a Wolverhampton Delivery Office a month earlier:

Screenshot by the author

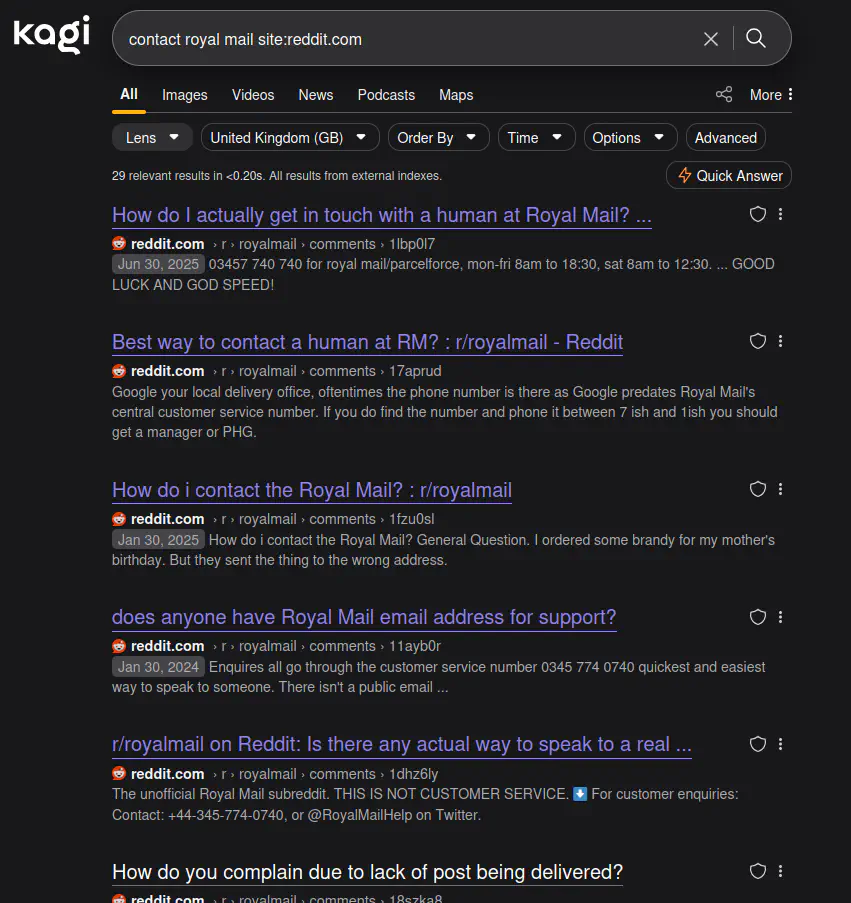

I searched around for how to contact Royal Mail support, to ask them what on earth they had done with my very important tax documents. This led me on several fruitless loops as I was unable to find any obvious asynchronous way to contact them:

I gave in, and tried to call a couple of the numbers I had alighted upon on separate journeys through the support page maze. Across six attempts, four automatically hung up on me and the other two had me on hold for thirty minutes apiece before I gave up. I searched online for contact details, which was were I discovered a flood of Reddit threads of people facing the same problems:

Screenshot by the author

In between what I can only describe as ‘telephone numerology’ and the appearance of one apparent Mail customer service representative, I finally found an unpublished customer support email address and submitted my enquiry; I received an automated reply saying they would try to get back to my within seven days.

In the meantime, I tried chewing the sausage from the other end and called HMRC. After an absolutely interminable slog through the automated chatbot and endless pre-recorded messages—with the end-of-January deadline looming, they really want everyone to know that if it’s not urgent they should come back in February—I actually got talking to someone surprisingly quickly. She confirmed that they had received the amended return (Great! I don’t need to interact with Royal Mail any more!), and that it was currently forecast to be processed in *tapatapatapatap* November.

(The astute reader shall, at this juncture, no doubt recognise that this is a ridiculous delay for processing an amendment of which they had been prewarned, and also absolutely no fucking use to me right now.)

She clearly had my amended return up on her computer screen as she referred to figures in it. So HMRC had my updated return, and it knew it had my updated return, but it wouldn’t officially know that it knew for the best part of a year, by which point it would have robbed me of the best part of ten grand that both it, and I, knew it would end up giving back to me anyway.

In light of this incredibly stupid situation, I asked the support agent how I could pay the minimal amount to avoid any penalties whilst I waited for their team of highly-trained sloths to finally get around to fixing my bill (obviously, not quite in those terms). I could set up a payment plan, but I would accrue interest on my outstanding balance that I would still have to pay off even after the balance from which the interest arose was nullified (as we both knew it would be). Even though the interest is non-compounding, I would still be looking at an additional £530. So, not an option.

This left me with only one course of action: come up with the cash by the end of January (which was, at this point, a few weeks away). That’s not exactly the kind of sum one carries around in their back pocket, but I was eventually able to sell off enough shares in my long-term savings to cover it.5

I fully appreciate that I am in a very fortunate financial position here,6 which just makes the phenomenal unnecessariness of this situation so frustrating: I’m sure many people, faced with a bill like this, would have to choose between either a) paying a £530 premium for the crime of poverty or b) taking out a loan, with all of the dangers of taking on such debt, which will persist long after the initial balance is all resolved.

Whilst I was (increasingly nervously) waiting to get access to my cash, I decided to take a closer look at the tax calculation to try and figure out how the bill—even accounting for my erroneous figures—had ended up so sizeable. At which point, something jumped out at me:

Photo by the author

Even with my wrong figures, I was only due to pay a few grand of tax. So why was I now looking at paying well over twice that? Well, just below the above calculation, was this one:

Photo by the author

Cuntsssssssssssssssssss…

But wait: I had dutifully informed the SLC when I moved abroad, and had set up a Direct Debit to make my monthly repayments. HMRC and the SLC are both government agencies, and when you work in the UK your loan repayments are automatically deducted from your payroll each month, so they clearly talk to each other. So why were they now double-charging me?

After some digging, I found this small note buried in one of their help pages (emphasis mine):

Overseas Direct Debit payments ¶

If you have been paying Direct Debit payments to the SLC while you have been abroad your tax return will need to include your total income.

Your student loan repayments will be calculated on this total income, but will not take into account the Direct Debit payments you have already made to the SLC.

After you send your tax return, contact the Student Loan Company and they will tell HMRC how much you have paid.

HMRC then uses this figure to reduce the amount of tax you owe.

So despite being two cheeks of the same arse, and despite information normally flowing bidirectionally and automatically between the two bodies, in this ONE specific case I have to (for some reason, unstated) contact the SLC to tell them to tell HMRC that I’ve been paying my loan off.

I called SLC. Another fucking phone maze. More waiting to the sound of classicial music through tinny mobile phone speakers. Another friendly enough support agent, forced to bear the brunt of my wholly justified frustration. She said she had passed on my request to their ‘backoffice team’, and it would be processed ‘in five working days’. Fuck off.

But the eagle-eyed reader will have noticed a £3,000-ish difference between the numbers I was being asked to pay, and the Income Tax that had been calculated. For this final piece of the puzzle, I had to dig a bit into the letter, where I found this:

Photo by the author

So despite me having repeatedly told them that this year was a one-off, and that I would be fully tax-resident in France next time with no tax obligations in the UK, these loveless jizztrumpets decided that what I meant to say was that I would in fact owe them another three grand in the next tax year, and would be happy to pay it in two instalments.

I have submitted a separate claim to reduce the predicted payments, but who knows how long it will be before anybody gets around to reviewing it.

I managed to pay my January bill with one day remaining. I was initially going to hold back the July instalment until the last moment in the hopes that the typewriter monkeys might manage to process my amendment before then, but now I think I’ll pay it off immediately—I just learnt that HMRC will pay you back with interest for early overpayment, and even though the interest rate is probably worse than I could get by just reinvesting the money, the small justice of squeezing it out of these fuckwits has an irresistable appeal.

I now have three separate claims in processing to try and regularise my bill:

I have been reassessing my relationship with my homeland, and this experience could not have come at a more febrile moment for me. I’m working on several (much longer) pieces that will delve deep into the details, but suffice it to say here that I have come to detest this wretched isle and all that it stands for; unfortunately, even a failing government tends to retain its ability to exort money until the very last.

It is impossible, however, to have a seven-grand hole blown out of your budget through a combination of bureaucratic incomprehensibility, unreasonable wait times and the lumbering administrative remnants of a failed attempt by a government long past to scam itself at the expense of future governments and future generations (and I’m not even talking about Brexit!). Those three things are the perfect trifecta of the contemporary British experience, and I want no more part in it.

On top of all that, by doing the quote-unquote ‘right thing’ and diligently making my loan repayments from overseas, I am in fact paying another premium due to the absurd figures used by the SLC to calculate overseas rates.7 As luck would have it, the SLC has historically shown neither the appetite nor the capability for chasing non-paying overseas graduates, and the only potential downside to non-payment is the accrual of punitive arrears which will have to be repaid if one ever returns to work in the UK; I think I would rather take a bath with my toaster. Although, of course, until and unless they decide to sell my loan, I will remain at the mercy of every subsequent government’s change of heart on this and all other terms of the loan. For now—whilst I value keeping my options open over an urgent need to save cash—I will keep up my repayments, but I have twenty more years of this to go and as soon as the egregiousness of actual present-day fuckery outweighs the risk of potential future fuckery, it’s reassuring to know that there is a big wide world out there to disappear into.

So, as I call time on my twenties and prepare to embark on my thirties with newfound and hard-won wisdom and sagacity, I’m finally starting—unhappily—to internalise the principal lesson that Britain has been teaching me all my life: only a sucker plays by the rules.

May I have fewest possible future dealings with any of these robbing bastards, or the rock they call home, for as long as I live.

Ireland was once in the same boat as us, until the IRA heroically fought for (and won) the right to a reasonable tax year (amongst, I think, some other things). ↩︎

Despite the faff, there are a few things I quite like about the French system: you get tax credit for union dues, for one; and a very generous 60% credit for charitable donations. ↩︎

I accept that this is where an accountant with cross-Channel expertise would have been handy. ↩︎

Actually, this was probably the first year I’ve begun without a hangover in as long as I can remember. I had a very wholesome night. I cooked a bouillebaisse for some friends and we danced some salsa. ↩︎

This actually brought its own sweatiness, as my Jan 23 request to sell didn’t actually go through until Jan 29. ↩︎

In fact, if the economy crashes between now and me reinvesting the money when I get it back, I may actually stand to make a tidy profit with this enforced trading. ↩︎

Actually—I had forgotten until just now—the fuckers also tried to slap me with £600 in ‘arrears’ when I got back from Central America, despite me having told them my travel dates and that I would have had no income. Another time, they demanded three months of unredacted bank statements to provide evidence of your financial means of support

; I sent them three for an account that I used for no transactions other than receiving money and immediately forwarding on, and they accepted that. ↩︎